Chapter 5 Forms of Market

1. Choose the correct option:

Question 1.

In an economic sense, the market includes the following activities

a) The place where goods are sold and purchased.

b) An arrangement through which buyers and sellers come in close contact with each other directly or indirectly.

c) A shop where goods are sold.

d) All of the above.

Options :

1) a and b

2) b and c

3) a, b and c

4) only b

Answer:

4) only b

Question 2.

Classification of markets on the basis of place

a) Local market, National market, International market

b) Very short period market, Local market, National market.

c) Short period market, National market, International market.

d) Local market, National market, Short period market.

Options :

1) a, b and c

2) b. c and d

3) only a

4) a and d

Answers:

3) only a

Question 3.

Homogeneous product is a feature of this market.

a) Monopoly

b) Monopolistic competition

c) Perfect competition

d) Oligopoly

Options:

1) c and d

2) a, b and c

3) a, c and d

4) only c

Answer:

4) only c

Question 4.

Under Perfect competition, sellers are

a) Price makers

b) Price takers

c) Price discriminators

d) None of these

Options:

1) a, b and c

2) only b

3) only c

4) a and c

Answers:

2) only b

2. Give economic terms:

1) The market where there are few sellers.

2) The point where demand and supply curve intersect.

3) The cost incurred by the firm to promote sales.

4) Number of firms producing identical product.

5) Charging different prices to different consumers for the same product or services.

Answers:

- Oligopoly

- Equilibrium point

- Selling cost

- Homogeneous

- Discriminating monopoly

3. Complete the Correlation:

1) Perfect competition : Free entry and exit :: ……………. : Barriers to entry.

2) Price taker …………….:: Price maker:: Monopoly.

3) Single price : Perfect competition :: Discriminated prices : …………….

Answers:

- Monopoly

- Perfect competition

- Monopoly

4. Find the odd word out:

1) Selling cost : Free gifts, Advertisement hoardings. Window displays. Patents.

2) Market sructure on the basis of competition : Monopoly. Oligopoly. Very Short Period market. Perfect competition.

3) Features of monopoly : Price maker, Entry barriers, Many sellers. Lack of substitutes.

4) Legal monopoly : Patent. OPEC. Copyright. Trade mark.

Answers:

- Free gift

- Very short period

- Many sellers

- OPEC

5. Answer the following:

Question 1.

Explain the features of Oligopoly.

Answer:

The term Oligopoly is derived from the Greek words ‘Oligo’ which means few and ‘Poly’ which means sellers. Hence, following are its features –

1. Many buyers and few sellers : There are many buyers and a few sellers or firms (may be five or six) who dominate the market and have major control over the price of a product.

2. Interdependence : Since the number of firms are less, any change in price, output, product etc. by one firm will affect the rival firms and will force them to change their price, output, etc. E.g. In case of Coke and Pepsi in soft drink market.

3. Selling cost or advertising : Each firm in order to sell more of its product takes aggressive steps to advertise or through free samples. This helps them to capture larger sales.

4. Barrier to entry : The firm can easily exit from the industry whenever it wants, but to enter a new industry it has certain entry barriers like government license, patent right, etc.

5. Uncertainty : There is a great uncertainty in this market if the rival firms join hands and may try to fight each other.

6. Lack of Uniformity : The firms may produce either homogeneous or differentiated products. Eg. In automobile industry, Maruti, Indica are examples of differentiated product but cooking gas of Bharat Petroleum and Hindustan Petroleum are examples of homogeneous product or pure oligopoly.

Question 2.

Explain the types of Monopoly.

Answer:

There are different types of monopoly as analysed below:

(1) Natural Monopoly : A natural monopoly arises when a particular type of natural resource is located in a particular region like petrol or crude oil in Gulf countries. Also natural advantages such as good location, business reputation, age – old establishment s etc., confer natural monopoly. Similarly, many professional skills, natural talents give monopoly power. E.g. A singer or actor has monopoly of his skill, talent.

(2) Legal Monopoly : Legal monopolies are those monopolies which are recognised by law. Legal protection granted by the Government in the form of trade mark, copy rights, license etc., give monopoly power to j the firms. Here the potential competitors are j not allowed to copy the product registered under the given brand names, patents or trade marks according to the law.

(3) Joint Monopoly or Voluntary Monopoly : This monopoly arises through mutual agreement and business combinations like the formation of cartels, syndicate, trust etc. For e.g. Oil producing nations have come together and formed a Cartel OPEC Organisation of Petroleum Exporting Countries.

(4) Simple Monopoly : A simple monopoly firm charges a uniform price for its product to all the buyers.

(5) Discriminating Monopoly : A discriminating monopoly firm charges different prices for the same product to ) different buyers. E.g. a doctor, a teacher, a lawyer, etc., charges different fees from the people. The practice of charging different j prices from different buyers is called “Price discrimination.”

(6) Private Monopoly : When an individual or a private firm enjoys the monopoly of manufacturing and supplying a particular product, it is called private monopoly. The main aim of private monopolist is profit maximisation.

(7) Public Monopoly : When a field of production is solely owned, controlled and operated by the government, it is regarded as public monopoly. Eg. Public utility service like Railways, Electricity, Water Supply etc. Since these monopolies are service motivated and welfare oriented they are also called welfare monopolies.

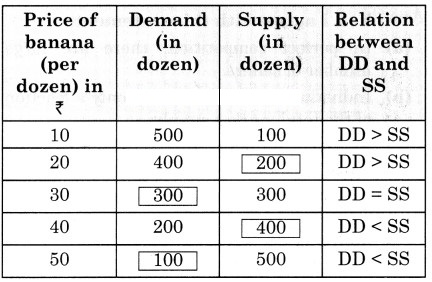

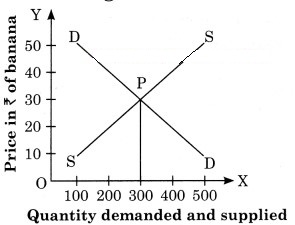

6. Observe the table and answer the questions:

Question 1.

Fill in the blanks in the above schedule.

Answer:

Question 2.

Derive the equilibrium price from the above schedule with the help of a suitable diagram.

Answer:

In the diagram, equilibrium price is ₹ 30/- because at this point dd curve insects SS curve at point ‘P’. At this point DD is 300 doz of bananas and sellers are ready to sell 300 doz at price ₹ 3.

7. Answer in detail:

Question 1.

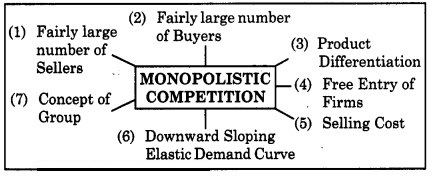

Explain the meaning of Monopolistic competition with its features.

Answer:

(1) Fairly large number of Sellers : There are large number of sellers selling closely related, but not identical products. There is tough competition among sellers. An individual seller supply is just a small part) of the total supply, so he has limited degree l of control over market supply and price. Each firm (seller) can formulate its own price and output policy independently.

(2) Fairly large number of Buyers: There are large numbers of buyers in a monopolistic competition market. Each buyer enjoys his preference over a particular brand and chooses to buy a specific brand of product. Hence, the buying is by choice and not by chance.

(3) Product Differentiation : The most distinguishing feature of monopolistic competition is that the product produced by different firms are not identical, they are slightly different from each other but they are close substitutes. The product differentiation can be done in different ways like may be in the form of brand names say Raymonds. It can be differentiated in terms of colour, size, design, etc., say soap, mobiles etc., or through sales technique. For e.g. cars, two wheelers, air conditioners, etc.

(4) Free Entry of Firms: A firm is free to enter the market as there are no entry barriers. Similarly there are no restrictions if the firm wants to quit the market. Freedom of entry leads to occurrence of only normal profit in the long run.

(5) Selling Cost : One of the special features of monopolistic competition is the selling cost. Selling costs are those costs, which are incurred by firms to create more and more demand for its products through advertisement, salesmanship, free samples, exhibitions, etc.

(6) Downward Sloping Elastic Demand Curve : The demand curve faced by each firm is downward sloping and comparatively more elastic. It implies that an individual firm can sell more only by reducing the price.

(7) Concept of Group : Under monopolistic competition, Prof. E. H. Chamberlin introduced the concept of group in place of Marshallian concept of industry. Industry means a number of firms producing identical products. A group means a number of firms producing differentiated product, which are close substitutes.

Question 2.

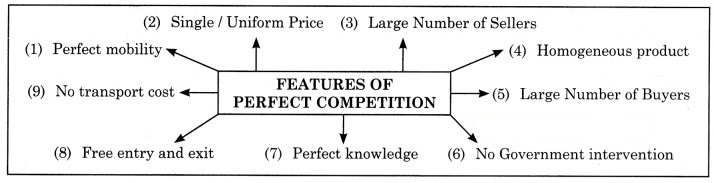

Explain the meaning of Perfect competition with its features.

Answer:

(1) Perfect Mobility of Factors of Production : Factors of production that is land, labour, capital are perfectly free to move from one firm to another or from one industry to another from one region to another or from one occupation to another. This ensures freedom of entry and exit for individuals and firms.

(2) Single / Uniform Price : There exists a single price for homogeneous product in the entire market at a given point of time. The price is determined by forces of demand and supply.

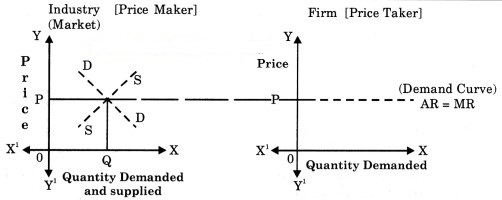

(3) Large Numbers of ellers : There are many sellers in this market. The number of sellers (firms) are so large that a single seller cannot influence the market price nor the total output in the market (Industry). The contribution of one seller is insignificant and microscopic. The price in the market is determined by the forces of market demand and market supply. Hence, a firm or seller is a ‘price taker’ and not a ‘price maker.’

(4) Homogeneous Product : The products produced by all the firms in the industry are identical and are perfect substitute to each other. The products are identical in shape, size, colour, etc. and hence uniform price rules the market for the product.

(5) Large Number of Buyers : There are large number of buyers in the market. One individual buyer’s demand is only a small fraction of total market demand so he is not in a position to influence the price. He is a price taker.

(6) No Government Intervention : It is assumed that the government does not interfere with the working of market economy. There are no tariffs, subsidies, licensing policy or other government interventions. This non – intervention of government is necessary to permit free entry of firms and automatic adjustment of demand and supply. In short, laissez faire policy prevails under perfect

(7) Perfect Knowledge : There is perfect knowledge on the part of buyers and sellers regarding the market conditions especially regarding market price. As a result no buyer will pay a higher price than the market price and no seller will charge a lower price than the market price. So a single price would prevail for a commodity in the entire market.

(8) Free Entry and Free Exit : There is freedom for new firms or sellers to enter the industry or market. There are no legal, j economic or any other type of restrictions or; barriers for new firms to enter the industry or an existing firms to quit the industry, Entry of new firm usually takes place j when existing firms enjoy abnormal profit. Similarly, existing firms quit the industry when they face losses.

(9) No Transport Cost: It is assumed that all firms are close to the market and hence there is no transport cost. If the transport cost are added to the price of product then the homogeneous commodity will have different prices depending upon the distance from the place of supply to the market.

Question 1.

Do you know?

What is monopsony?

Answer:

Monopsony is opposite of monopoly market but it is rarely found in reality.

In monopsony, there are large number of sellers but buyer is only one. So buyer has complete control over the price in the market. He can bargain with the sellers and fix the price at his terms.

Find out (Textbook Page 50)

What are the types of monopoly of the following products or services and give reason.

(1) Tea in Assam, (2) Atomic energy, (3) Logo of a commercial bank

Answer:

Find out (Textbook Page 51)

Find the close substitutes for the following products:

Answer: