Chapter 8 Rectification of Errors

1. Answer in One Sentence:

Question 1.

What is meant by rectification of errors?

Answer:

The correction of accounting errors in a systematic manner is called the rectification of errors.

Question 2.

What is meant by the error of principle?

Answer:

An error committed by the accountant by not following accounting principles properly is called an error of principle.

Question 3.

What is meant by the error of partial omission?

Answer:

An error in which a transaction is correctly recorded in the books of account but one of the postings is wrong is known as partial omission. If will affect the trial balance.

Question 4.

What is meant by the error of complete omission?

Answer:

Failure on the part of an accountant to record the business transactions in the books of account is called an error of complete omission. It does not affect the agreement of the trial balance.

Question 5.

What are compensating errors?

Answer:

The error which is committed on one side of the ledger account compensates for an error committed on the other side of some other leader account is called compensating error.

2. Give one word/term or phrase for each of the following statements.

Question 1.

Errors that affect the agreement of Trial Balance.

Answer:

One-sided errors

Question 2.

Taking the total more while closing books of accounts.

Answer:

Overcasting

Question 3.

The error arises when a transaction is partially or completely omitted to be recorded in the books of accounts.

Answer:

Error of omission

Question 4.

Transactions recorded due to violating of the accounting principles.

Answer:

Error of principle

Question 5.

Accounts to which difference in Trial Balance is transferred.

Answer:

Suspense account

Question 6.

Error in which the effect of one mistake is nullified by another mistake.

Answer:

Compensating error

Question 7.

Errors that are not disclosed by the Trial Balance.

Answer:

Two-sided errors

Question 8.

Errors of incorrect entries or wrong posting.

Answer:

Errors of commission

3. Select the most appropriate alternative from those given below and rewrite the sentence.

Question 1.

Rectification entries are passed in ______________

(a) Journal Proper

(b) Ledger

(c) Balance Sheet

(d) Cash Book

Answer:

(a) Journal Proper

Question 2.

The type of error for which journal entry is always required for rectification ______________

(a) over casting

(b) one sided error

(c) under casting

(d) two sided error

Answer:

(d) two-sided error

Question 3.

Error occurred due to wrong posting are called error of ______________

(a) principal

(b) commission

(c) compensating

(d) omission

Answer:

(b) commission

Question 4.

If transaction is totally omitted from the books, it is called ______________

(a) Error of recording

(b) Error of omission

(c) Error of principle

(d) Error of commission

Answer:

(b) Error of omission

Question 5.

Suspense Account is opened when ______________ does not tally.

(a) Balance sheet

(b) Trading Account

(c) Profit and loss

(d) Trial Balance

Answer:

(d) Trial Balance

4. State whether the following statements are True or False with reasons.

Question 1.

Trial Balance is prepared from the balance of ledger accounts.

Answer:

This statement is True.

A Trial balance is a statement of debit and credit balances extracted from the various accounts in the ledger. All business transactions are recorded first in Journal or in subsidiary books and subsequently, they are posted to respective ledger accounts. At the end of the year, they are balanced and transferred to the Trial balance.

Question 2.

A Trial Balance can agree in spite of certain errors.

Answer:

This statement is True.

The error of principle or error of complete omission or compensatory error is not disclosed by the Trial Balance. It will be agreed with debit and credit balances but there may be a certain error.

Question 3.

Rectification entries are passed in Cash Book.

Answer:

This statement is False.

Rectification entries are passed in the Journal Proper book. Cashbook is mainly used for cash transactions and not for rectification of errors.

Question 4.

There is no need to open a Suspense Account if the Trial Balance agrees.

Answer:

This statement is True.

When the Trial Balance does not tally a temporary account called ‘Suspense Account’ is opened to balance the trial balance. So when the trial balance is agreed there is no need to open ‘Suspense Account’.

Question 5.

All the errors can be rectified only through Suspense Account.

Answer:

This statement is False.

The errors of principle and errors of complete omission can be rectified by passing entries. So all the errors can not be rectified by the Trial Balance.

5. Do you agree or disagree with the following statements.

Question 1.

The unintentional omission or commission of amounts and accounts while recording the transactions is known as an error.

Answer:

Agree

Question 2.

The errors committed due to wrong recording, wrong posting, wrong totaling, wrong balancing, wrong calculations are known as Arithmetical errors.

Answer:

Disagree

Question 3.

When one or more debit errors happen to equal one or more credit errors it is said to be a Compensating error.

Answer:

Agree

Question 4.

The agreement of Trial balance is not affected when a transaction is not recorded at all in the original Books.

Answer:

Agree

Question 5.

When a transaction is not recorded according to the principles of accounting it is known as Compensating error.

Answer:

Disagree

6. Complete the following sentence.

Question 1.

______________ is assured only when there are no errors in the books of accounts.

Answer:

Accuracy

Question 2.

Transactions recorded in contravention of the accounting principles are known as ______________

Answer:

errors of principle

Question 3.

______________ entry depends generally on when the error is detected.

Answer:

Rectifying

Question 4.

Temporary account opened to rectify the entry is known as ______________

Answer:

suspense account

Question 5.

Errors are caused due to ______________ recording of transactions.

Answer:

wrong

Practical Problems

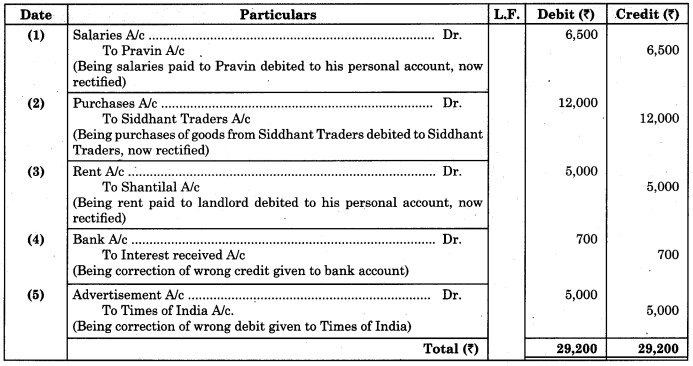

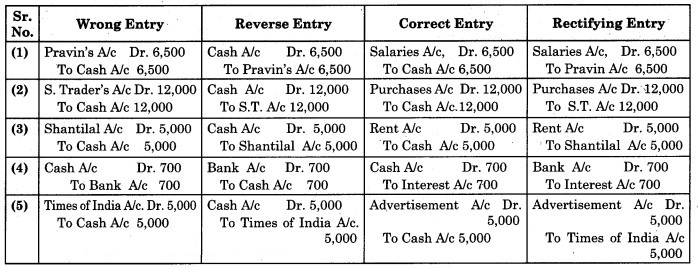

Question 1.

Rectify the following errors:

1. Salary paid to Pravin was wrongly debited to his personal account ₹ 6,500/-

2. Cash Purchases ₹ 12,000/- from Siddhant Traders was debited to Siddhant Trader Account.

3. Paid Rent ₹ 5,000 to landlord Shantilal was debited to his personal account.

4. Received interest ₹ 700 from Bank was wrongly credited to Bank Account.

5. Advertisement expenses ₹ 5,000/- paid to Times of India was debited to Times of India.

Solution:

Journal Proper

Working Note:

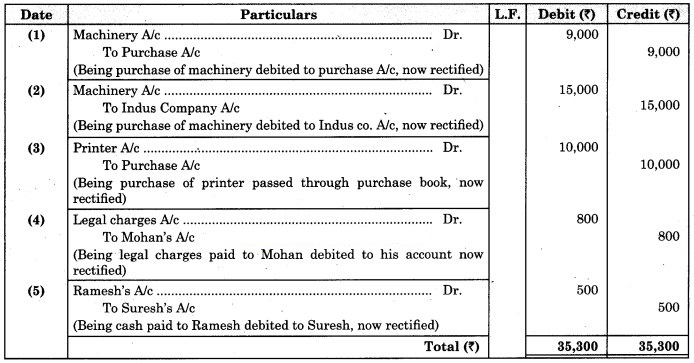

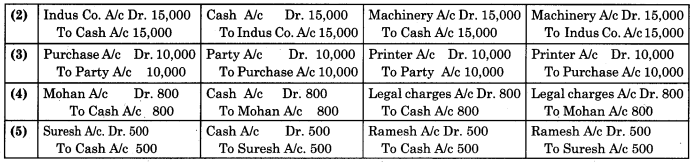

Question 2.

Rectify the following errors:

1. Machinery purchased for ₹ 9,000/- has been debited to Purchase Account.

2. ₹ 15,000/- paid to Indus Company for Machinery purchased stand debited to Indus Company Account.

3. Printer Purchased for ₹ 10,000/- was wrongly passed through Purchase Book.

4. ₹ 800/- paid to Mohan as Legal Charges were debited to his personal account.

5. Cash paid to Ramesh ₹ 500/- was debited to Suresh.

Solution:

Journal Proper

Working Note:

Question 3.

Rectify the following errors:

1. A credit sale of goods to Sanjay ₹ 3,000/- has been wrongly passed through the ‘Purchase Book’.

2. A credit purchase of goods from Sheetal amounting to ₹ 2,000/- has been wrongly passed through the ‘Sales Book’.

3. A return of goods worth ₹ 500/- to Umesh was passed through the ‘Sales Return Book’.

4. A return of goods worth ₹ 900/- by Ganesh was entered in ‘Purchase Return Book’.

5. Credit Purchases from Neha ₹ 10,000/- were recorded as ₹ 11,000/-

Solution:

Journal Proper

Working Note:

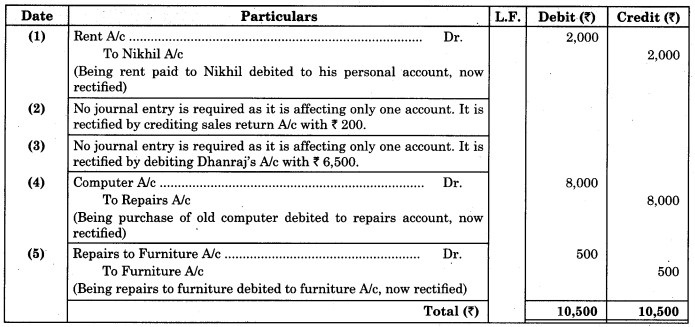

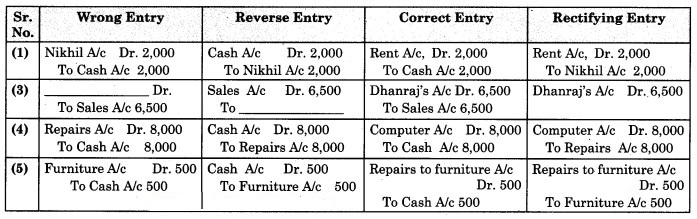

Question 4.

Rectify the following errors:

1. Paid Rent ₹ 2,000/- to Nikhil has been debited to his personal account.

2. Total of the Sales Return Book is wrongly taken more by ₹ 200/-

3. Goods sold to Dhanraj ₹ 6,500/- on credit were not posted to his personal account.

4. Old Computer purchased was debited to Repairs account ₹ 8,000/-

5. Repairs to Furniture of ₹ 500/- have been debited to Furniture account.

Solution:

Journal Proper

Working Note:

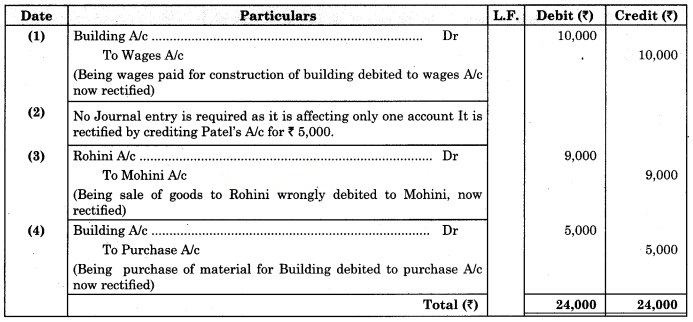

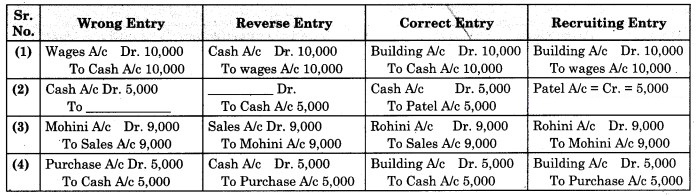

Question 5.

Rectify the following errors:

1. Wages paid for the construction of Building ₹ 10,000/- was wrongly debited to Wages Account.

2. Cash received from Patel ₹ 5,000/- though recorded in Cash Book was not posted to his personal account in the Ledger.

3. Sold goods worth ₹ 9,000/- to Rohini has been wrongly debited to Mohini’s Account.

4. Material purchased for construction of Building was debited to Purchase Account ₹ 5,000/-

Solution:

Journal Proper

Working Note:

Question 6.

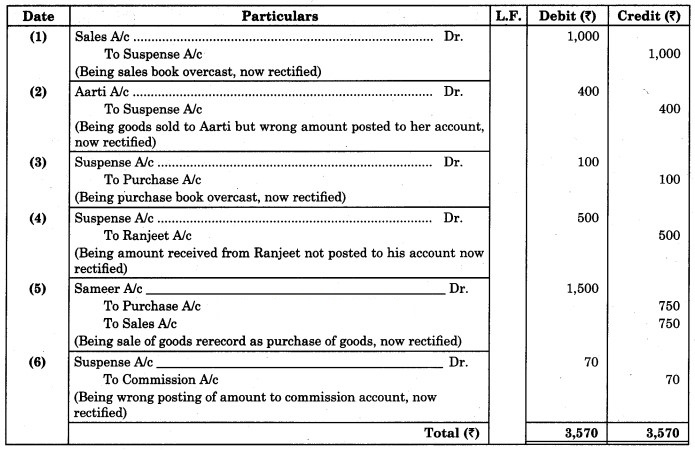

There was a difference of ₹ 1230/- in a Trial Balance. It was placed on the Debit side of Suspense A/c. Later on, the following errors were discovered. Pass rectifying entries and prepare Suspense A/c.

1. Sales Book was overcast by ₹ 1,000/-

2. Goods sold to Aarti for ₹ 4,400/- has been posted to her account as ₹ 4,000/-

3. Purchases Book was overcast by ₹ 100/-

4. An amount of ₹ 500/- received from Ranjeet, has not been posted to his account.

5. Goods sold to Sameer for ₹ 750/- were recorded in Purchase Book.

6. An amount of ₹ 500/- has been posted to the credit side of the Commission Account instead of ₹ 570/-

Solution:

Journal Proper

Question 7.

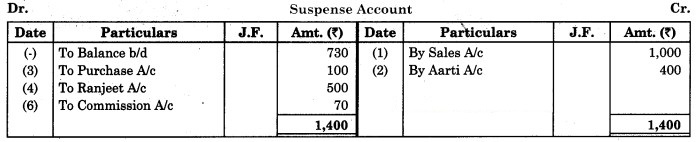

A bookkeeper finds that the debit side of the Trial Balance is short of ₹ 308/- and so for the time being, the balances of the side by putting the difference to Suspense Account. The following errors were disclosed.

1. The debit side of the purchases account was undercast by ₹ 100/-

2. ₹ 100/- is the monthly total of discount allowed to customers were credited to the discount account in the ledger.

3. An entry for goods sold of ₹ 102/- to Mihir was posted to his account as ₹ 120/-

4. ₹ 26/- appearing in the Cash Book as paid for the purchase of Stationery for office use have not been posted to Ledger.

5. ₹ 275/- paid by Mihir were credited to Mithali’s Account.

You are required to make the necessary Journal Entries and the Suspense Account.

Solution:

Journal Proper

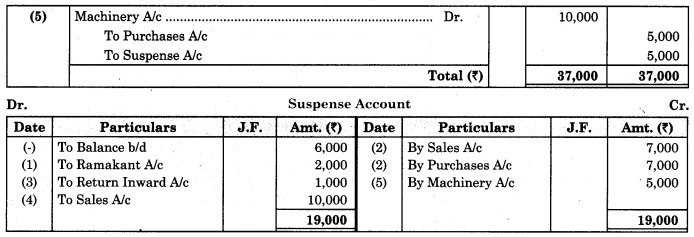

Question 8.

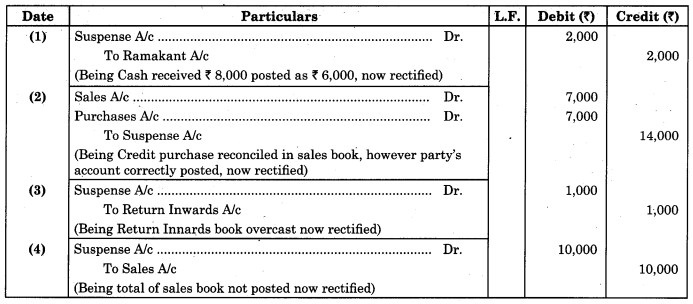

The trial Balance of Anurag did not agree. It showed an excess credit of ₹ 6,000/-. He put the difference to Suspense Account. He discovered the following errors.

1. Cash received from Ramakant ₹ 8,000/- posted to his account as ₹ 6,000/-

2. Credit purchases from Naman ₹ 7,000/- were recorded in Sales Book. However, Naman’s Account was correctly credited.

3. Return Inwards Book overcast by ₹ 1,000/-

4. Total of Sales Book ₹ 10,000/- was not posted to Sales Account.

5. Machinery purchased for ₹ 10,000/- was posted to Purchases Account as ₹ 5,000/-.

Rectify the errors and prepare Suspense Account.

Solution:

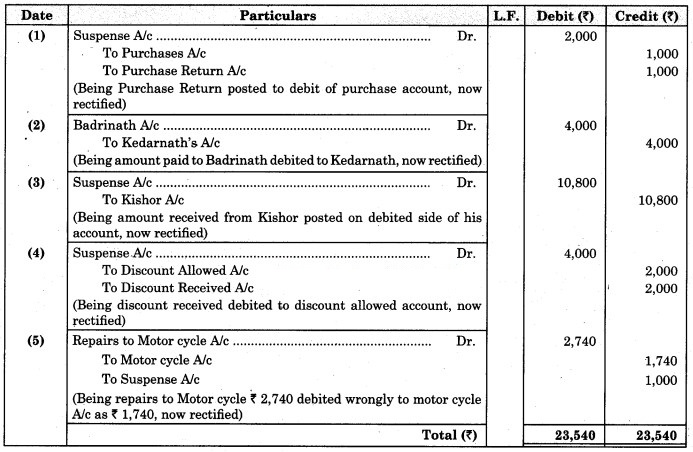

Question 9.

There was an error in the Trial Balance of Mr. Yashwant on 31st March 2019, and the difference in Books was carried to a Suspense Account. Ongoing through the Books you found that.

1. ₹ 1,000/- being purchases return were posted to the debit of Purchase Account.

2. ₹ 4,000/- paid to Badrinath was debited to Kedarnath’s Account.

3. ₹ 5,400/- received from Kishor was posted to the debit of his account.

4. Discount received ₹ 2,000/- was posted to the debit of Discount Allowed Account.

5. ₹ 2,740/- paid to Repairs to Motor Cycle was debited to Motor Cycle Account ₹ 1,740/-

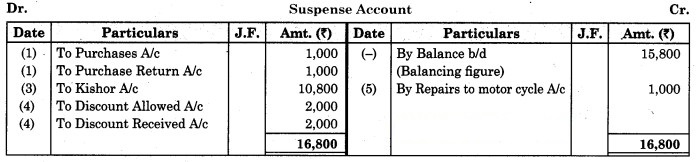

Give Journal Entries to rectify the above errors and ascertain the amount transferred to Suspense Account on 31st March 2019 by showing the Suspense Account, assuming that the Suspense Account is balanced after the above corrections.

Solution:

Journal Proper

Question 10.

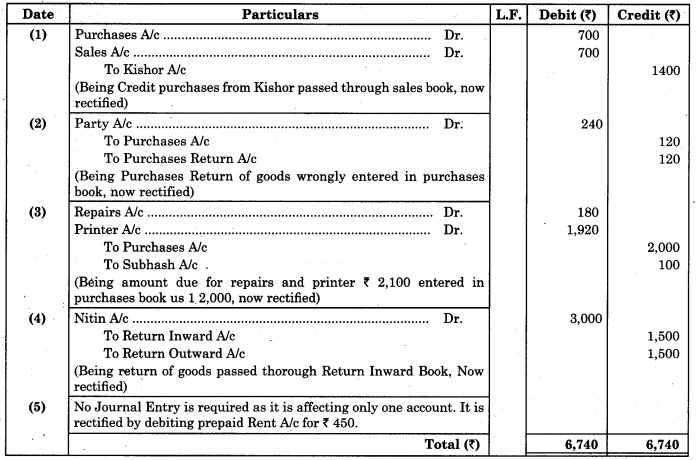

Rectify the following errors.

1. Goods purchased from Kishor ₹ 700/- were passed through Sales Book.

2. An item of ₹ 120/- in respect of purchase returns, has been wrongly entered in the Purchase Book.

3. Amount payable to Subhash for repairs done to Printer ₹ 180/- and new Printer supplied for ₹ 1,920/-, were entered in the Purchase Book as ₹ 2,000/-

4. Returned goods to Nitin ₹ 1,500/- was passed through Returns Inward Book.

5. An item of ₹ 450/- relating to the Prepaid Rent account was omitted to be brought forward.

Solution:

Journal Proper

Note: In entry No. 5 Suspense A/c is not used as the problem is silent about the opening of Suspense A/c.